- Details

- Category: บทความทั่วไป

- Published: Sunday, 18 September 2016 11:09

- Hits: 4563

หุ่นยนต์ไทย…ความท้าทายใหม่ที่ น่าจับตามอง

Highlight

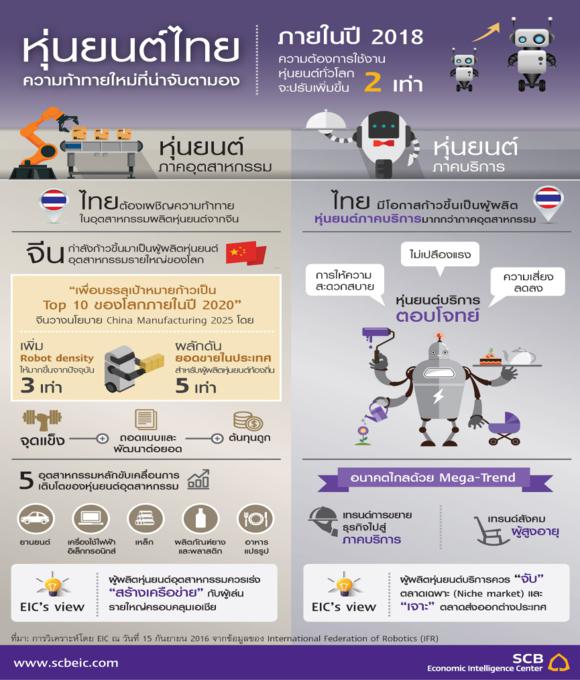

ในปัจจุบันหุ่นยนต์ถูกใช้งานกั บภาคอุตสาหกรรมเป็นส่วนใหญ่ แต่มีแนวโน้มจะหันไปใช้ในภาคบริ การมากขึ้นในอนาคต หากนับจากนี้ไปอีก 2-3 ปี ความต้องการใช้หุ่นยนต์ทั่ วโลกมีโอกาสที่จะปรับตัวเพิ่มขึ้ นอีกเกือบ 2 เท่า เป็นผลมาจากพฤติกรรมของผู้บริ โภคที่เริ่มเปลี่ยนไป ประกอบกับภาคอุตสาหกรรมต้ องการที่จะแก้ปั ญหาแรงงานขาดแคลนและพัฒนาขี ดความสามารถในการแข่งขันผ่ านการเพิ่มผลิตภาพอย่างต่อเนื่ อง ซึ่งในระยะต่อไปไทยอาจจะต้ องเผชิญกับความท้าทายจากจีนในอุ ตสาหกรรมการผลิตหุ่นยนต์อุ ตสาหกรรม เนื่องจากจีนกำลังจะก้าวขึ้ นมาเป็นผู้ที่มีบทบาทสำคัญในอุ ตสาหกรรมนี้ ดังนั้น อีไอซีมองว่าการเร่งสร้างเครื อข่ายพันธมิตรกับจีน รวมถึงผู้เล่นรายใหญ่อื่นๆ ให้ครอบคลุมทั้งภูมิภาคเอเชีย อาทิ เกาหลีใต้ ญี่ปุ่น ไต้หวัน เป็นสิ่งที่ไทยไม่ควรมองข้าม อย่างไรก็ดี สำหรับโอกาสและศั กยภาพของไทยในการผลิตหุ่นยนต์ บริการควรที่จะมุ่งเน้น การ “จับ” ตลาดเฉพาะ (niche market) และการ “เจาะ” ตลาดส่งออก (exports)

การใช้งานหุ่นยนต์ในภาคบริการมี แนวโน้มที่จะเพิ่มขึ้นในอนาคต ขณะที่การใช้งานหุ่นยนต์ในปัจจุ บันยังอยู่ในภาคอุตสาหกรรมเป็ นส่วนใหญ่ โดยงานที่ไม่ค่อยมีความซับซ้ อนมากนัก จะใช้ระบบอัตโนมัติ (automation) เพื่อควบคุมให้หุ่นยนต์ สามารถทำงานได้เองผ่านการเขี ยนโปรแกรม ในขณะที่หากงานมีความซับซ้อนสู งขึ้นจะใช้ปัญญาประดิษฐ์ (Artificial Intelligence) เข้าช่วยควบคุมเพื่อให้หุ่นยนต์ สามารถคิดเองได้ ซึ่งในช่วง 3 ปีที่ผ่านมานั้น ยอดขายเฉลี่ยต่อปีของหุ่นยนต์ บริการ (service robots) และหุ่นยนต์อุตสาหกรรม (industrial robots) ทั่วโลก มีอยู่ราว 5 ล้านตัว และ 2 แสนตัว ตามลำดับ โดยในปี 2018 International Federation of Robotics (IFR) คาดว่าการใช้งานหุ่นยนต์ ของโลกมีแนวโน้มที่จะเพิ่มขึ้ นอีกเกือบ 2 เท่า ซึ่งพฤติกรรมผู้บริโภคที่เปลี่ ยนไปในปัจจุบันจะส่งผลให้หุ่ นยนต์บริการได้รับความนิยมมากขึ้ นตามลำดับ ทั้งนี้ ผู้บริโภคเริ่มหันมาสนใจและใช้ งานหุ่นยนต์บริ การแทนการทำงานบางอย่างมากขึ้น เพื่อความสะดวกสบายที่เพิ่มขึ้น โดยที่ไม่ต้องทำงานที่เปลืองแรง หรืองานที่มีความเสี่ยงมากเกิ นไป เช่น การใช้หุ่นยนต์ดูดฝุ่ นแทนการทำความสะอาดบ้าน การใช้หุ่นยนต์ดูแลผู้สูงอายุ หรือการใช้หุ่นยนต์กู้ระเบิด เป็นต้น ขณะที่แรงขับเคลื่อนของความต้ องการใช้หุ่นยนต์อุ ตสาหกรรมจะมาจาก 5 อุตสาหกรรมหลัก ซึ่งมีสัดส่วนการใช้งานรวมกั นกว่า 85% ของการใช้งานหุ่นยนต์อุ ตสาหกรรมทั่วโลก (รูปที่ 1) อย่าง อุตสาหกรรมยานยนต์ เครื่องใช้ไฟฟ้าและอิเล็กทรอนิ กส์ เหล็ก ผลิตภัณฑ์ยางและพลาสติก และการแปรรูปอาหาร เพื่อแก้ปัญหาด้ านแรงงานขาดแคลนและพัฒนาขี ดความสามารถในการแข่งขันของอุ ตสาหกรรมผ่านการเพิ่มผลิตภาพ โดยมีจีนเป็นผู้เล่นอันดับ 1 ที่มีความต้องการใช้งานหุ่นยนต์ อุตสาหกรรมมากที่สุดในโลก ซึ่งครองสัดส่ วนของยอดขายในตลาดโลกไปแล้วกว่า 30% และยังมีแนวโน้มจะเพิ่มขึ้นอี กในอนาคต

ปัจจุบันจีนกำลังจะพัฒนาตนเองขึ้ นมาเป็นผู้ผลิตหุ่นยนต์อุ ตสาหกรรมรายใหญ่ของโลกซึ่งจะส่ งผลให้จีนกลายเป็นผู้ที่มี บทบาทสำคัญในอุตสาหกรรมนี้ ในระยะต่อไป แม้ว่าปัจจุบันยอดขายหุ่นยนต์อุ ตสาหกรรมในจีนจะมีมากที่สุ ดในโลก แต่เมื่อมองที่อัตราส่ วนการแทนที่ของหุ่นยนต์ต่ อจำนวนแรงงาน (robot density) ในจีน เมื่อปี 2015 พบว่ายังมีอัตราส่วนที่ค่อนข้ างน้อย ซึ่งอยู่แค่ราว 36 ตัวต่อแรงงาน 10,000 คน ถือว่าอยู่ในระดับที่ต่ำกว่าค่ าเฉลี่ยโลกเกือบเท่าตัว อีกทั้งยังไม่ติด 1 ใน 20 ของประเทศที่มี robot density มากที่สุด (รูปที่ 2) โดยล่าสุดรัฐบาลจีนตั้งเป้ าหมายว่าภายในปี 2020 นั้น จีนจะเพิ่ม robot density ให้สูงขึ้นอีกกว่า 300% เป็น 150 ตัวต่อแรงงาน 10,000 คน รวมถึงจะผลักดันให้ผู้ผลิตหุ่ นยนต์ท้องถิ่นมี ยอดขายในประเทศที่เพิ่มขึ้นอี กกว่า 5 เท่าตัวจากในปี 2015 ที่มีอยู่แค่ราว 2 หมื่นตัว ภายใต้นโยบาย China Manufacturing 2025 ที่จะสร้างอุตสาหกรรมการผลิตหุ่ นยนต์อุตสาหกรรมให้เป็น 1 ใน 10 อุตสาหกรรมเป้าหมายของจีน ทั้งนี้ ผู้ประกอบการจีนก็เริ่มมี ความเคลื่อนไหวเชิงสนับสนุ นนโยบายอย่างต่อเนื่อง อาทิ กรณีที่บริษัท Media ผู้ผลิตเครื่องใช้ไฟฟ้าจีนรายใหญ่เข้าซื้อกิจการของ Kuka ผู้ผลิตหุ่นยนต์อุ ตสาหกรรมรายใหญ่ของโลก หรือกรณีที่บริษัท Ningbo Techmation ผู้ผลิตเครื่องจักรผลิตพลาสติ กจีนรายใหญ่ได้จัดตั้งบริษั ทใหม่อย่าง E-Deodar ขึ้นมาเพื่อผลิตหุ่นยนต์ให้ ราคาถูกกว่าบริษัทต่างชาติอย่าง Kawasaki Robotics อย่างไรก็ตาม แม้ว่าปัจจุบันจีนจะยังไม่มี องค์ความรู้ (know-how) ในการที่จะผลิตหุ่นยนต์ แต่จีนมีศักยภาพในด้ านการถอดแบบและพัฒนาต่อยอดผลิ ตภัณฑ์โดยใช้ต้นทุนที่ต่ำกว่ าหลายประเทศมาก จึงมีความเป็นไปได้ค่อนข้างสู งที่จีนจะสามารถก้าวขึ้นมาเป็ นผู้ผลิตหุ่นยนต์อุ ตสาหกรรมรายใหญ่ของโลกได้ ในอนาคต ซึ่งในปัจจุบันไทยก็กำลังจะสร้ างอุตสาหกรรมหุ่นยนต์ขึ้นมาใหม่ ด้วยเช่นกัน เพื่อสร้างแรงขับเคลื่อนอุ ตสาหกรรมไทยไปสู่ยุค Thailand 4.0

ไทยอาจจะต้องเผชิญกับความท้ าทายจากจีนในอุตสาหกรรมการผลิ ตหุ่นยนต์อุตสาหกรรมแต่อีไอซี มองว่าไทยยังมีโอกาสและศั กยภาพในส่วนของการเป็นผู้ผลิตหุ่ นยนต์ภาคบริการ แม้ว่ายอดขายหุ่นยนต์อุ ตสาหกรรมในไทยสำหรับช่วง 2-3 ปีข้างหน้านี้จะมีแนวโน้มปรับตั วเพิ่มขึ้นอีกเกือบ 2 เท่า เมื่อเทียบกับยอดขายในปีที่ผ่ านมาซึ่งมีอยู่แค่ราว 4,000 ตัว แต่เมื่อมองในภูมิภาคนี้ไทยยั งถือว่าเป็นตลาดที่ค่อนข้างเล็ กอยู่ (รูปที่ 3) ดังนั้น ความเป็นไปได้ของไทยในการจะผั นตัวจากผู้ใช้ไปเป็นผู้ผลิตหุ่ นยนต์อุตสาหกรรมยังมีไม่สู งมากนัก เมื่อเทียบกับการที่จะขึ้นเป็ นผู้ผลิตหุ่นยนต์บริการที่ยั งพอเห็นโอกาสและความเป็นไปได้ มากกว่า จากแนวโน้มการเข้าสู่ยุคสังคมผู้ สูงอายุ ประกอบกับภาคอุตสาหกรรมเริ่ มขยายธุรกิจไปสู่ภาคบริการมากขึ้ น รวมถึงพฤติกรรมของผู้บริโภคก็ เปลี่ยนไปดังที่กล่าวไปแล้วข้ างต้น นอกจากนี้ ไทยยังมีความพร้อมในด้านทั กษะเชิงเทคนิคของบุ คลากรในประเทศ โดยเห็นได้จากผลงานของนิสิตนั กศึกษาไทยที่สามารถคว้ารางวั ลการประกวดหุ่นยนต์บริการในระดั บโลกได้มากมายหลายรายการ เพียงแต่ต้องมีการสนับสนุนจากทุ กภาคฝ่ายเพื่อที่จะพัฒนาต่ อยอดโครงการที่ประสบความสำ เร็จไปในเชิงพาณิชย์ให้มากขึ้นอย่ างต่อเนื่อง ซึ่งจะเป็นหนึ่งในปัจจัยที่ช่ วยสร้างโอกาสให้กับวงการอุ ตสาหกรรมหุ่นยนต์ไทยได้ในระยะต่ อไป

อีไอซีแนะผู้ผลิตหุ่นยนต์บริ การควรที่จะ 'จับ' ตลาดเฉพาะ (niche market)และ'เจาะ'ตลาดต่างประเทศผ่ านการส่งออกเพื่อให้ได้ การประหยัดต่อขนาด เช่น หุ่นยนต์ดินสอ (DINSAW) ของไทย เป็นกรณีศึกษาที่ประสบความสำเร็ จกรณีหนึ่งที่มีกลยุทธ์ ทางการตลาดชัดเจน รวมถึงพัฒนาหุ่นยนต์มาถูกทาง ไม่ว่าจะเป็นการพัฒนาหุ่นยนต์ เพื่อใช้ในภาคบริการและจั บตลาดเฉพาะอย่างตลาดผู้สูงอายุ รวมถึงการวางเป้าหมายในการที่ จะเจาะตลาดต่างประเทศหลักอย่ างญี่ปุ่นและสวีเดน เพื่อสร้างความเชื่อมั่นให้ตั วผลิตภัณฑ์และสร้างความเชื่ อใจให้ผู้บริโภค นอกจากนี้ หากเจาะตลาดทั้งสองประเทศนี้ สำเร็จก็ยังสามารถที่จะต่ อยอดไปสู่ตลาดส่งออกอื่นๆ ได้อีกด้วย ซึ่งจะทำให้ได้การประหยัดต่ อขนาดเพิ่ม

สำหรับ ผู้ผลิตหุ่นยนต์อุ ตสาหกรรมควรเร่งสร้างเครือข่ ายพันธมิตรกับผู้เล่นรายใหญ่ให้ ครอบคลุมทั้งเอเชียเพื่อพั ฒนาความแข็งแกร่งของห่วงโซ่อุ ปทานในภูมิภาคนี้ แม้ว่าปัจจุบันผู้ผลิตหุ่นยนต์ อุตสาหกรรมรายใหญ่จะอยู่ทางฝั่ งตะวันตก แต่หากมองถึงความพร้อมของตลาดที่ มีแนวโน้มจะเติบโตขึ้น ประกอบกับศักยภาพที่ มากพอในการที่จะผันตัวไปสู่ การเป็นผู้ผลิตหุ่นยนต์อุ ตสาหกรรมของโลกในอนาคต อีไอซีมองว่าผู้เล่นรายใหญ่ ในเอเชียไม่ว่าจะเป็นจีน ญี่ปุ่น เกาหลี ไต้หวัน ถือว่าเป็นผู้เล่นสำคัญที่ผู้ ผลิตไทยควรที่จะเข้าหาเพื่อสร้ างเครือข่ายในเชิงพันธมิตรไม่ ใช่เชิงการแข่งขัน เพื่อพัฒนาให้ห่วงโซ่อุปทานหุ่ นยนต์เคลื่อนมาอยู่ในภูมิภาคนี้ มากขึ้นในระยะต่อไป นอกจากนี้ ความพร้อมในห่วงโซ่อุปทานของอุ ตสาหกรรมอื่นๆ ที่สามารถจะพัฒนาต่อยอดไปสู่อุ ตสาหกรรมการผลิตหุ่นยนต์อุ ตสาหกรรม ไม่ว่าจะเป็นอุตสาหกรรมชิ้นส่ วนยานยนต์ ชิ้นส่วนเครื่องใช้ไฟฟ้าและอิ เล็กทรอนิกส์ หรือสินค้าที่มีเทคโนโลยีขั้นสู งก็มีการกระจุกอยู่ในภูมิภาคนี้ เป็นส่วนใหญ่

Robotics…new challenges to watch out for in Thailand

Highlight

Robotics has traditionally been used in the manufacturing sector, but the service sector will likely increase its use of robotics in the future. In the next couple of years global demand for robotics may double partly due to changing consumer behavior. Moreover, the manufacturing sector needs a solution to the labor shortage problem and to boost productivity in the face of increased competition. Going forward, challenges for

Thailand’s robotics industry may arise as China’s industrial robotics is becoming an influential player in the industry. Given that, EIC suggests Thai players quickly form an alliance with the Chinese and other key regional players in Asia such as South Korea, Japan, and Taiwan. Moreover, opportunities and potential for Thailand are particularly evident in service robotics, with a focus on serving niche markets and increasing exports.

Service sector robotics will gain momentum in the future while robotics is currently mainly used in the manufacturing sector. Less sophisticated processes can now rely on automation using robots to perform tasks for which they are programmed. The more sophisticated ones employ artificial intelligence (AI), which allows them to think and reason. During the past three years, average global sales of service and industrial robots were 5 million and 0.2 million units, respectively. According to the International Federation of Robotics (IFR), the use of robots will almost double by 2018. Changing consumer behavior is one factor, attributed to the increased popularity of service robots. Consumers have become interested in using robots to replace certain tasks because they seek more convenience, for labor-intensive tasks, or for risky activities. Examples include vacuum cleaners, robots to assist the elderly, and search-and-rescue robots or those dealing with bombs. As for industrial robots, demand drivers will come from five main industries that are potentially robot-intensive: the automotive, electronics and electrical appliances, metals, rubber and plastics, and food industries. Robots in these five industries now account for 85% of total robotic applications around the world (Figure 1). Robots have played a role in alleviating labor shortage problems and improving industrial competitiveness by raising productivity. Indeed, China is the number one robotics market, with the world highest demand for industrial robots. Chinese demand accounts for more than 30% of the market and is still on the rise.

China is now set to be the world’s major robot producer and continues to influence this industry. Despite the highest robotics sales in the world, China’s robot density (the ratio of robot units to employees) is still small. In 2015 robot density in China was only 36 units to 10,000 employees, just half the world’s average ratio. In fact, China’s ratio is not within top the 20 automation countries (Figure 2). The Chinese government recently declared a goal of raising its robot density 300% by 2020. This will bring China’s robot density to 150 units per 10,000 employees. Moreover, under the “China Manufacturing 2025” policy, the government wishes to increase sales of locally manufactured robots by five times, from around 20,000 units in 2015. This policy aims to make the robotics industry one of China’s 10 targeted industries. Chinese businesses have reacted positively to this policy. For example, large electrical appliance manufacturer Media Group acquired Kuka, one of the world’s largest industrial robotics producers. Ningbo Techmation, China’s major producer of machinery in the plastics industry, formed a new company “E-Deocar” to manufacture robots at a lower cost than foreign firms such as Kawasaki Robotics. In addition, while China is not yet equipped with the know-how technology to manufacture robots, it has the potential to reverse engineering and make improvements at significantly lower cost than other countries. It is therefore possible that China will step up to be the world’s major robot manufacturer in the near future. Thailand is also building its robotics industry to drive Thai industries towards the Thailand 4.0 era.

Thailand may face challenges from China, yet EIC sees Thai opportunities and potential in service robots. Even though sales of industrial robots in Thailand are expected to double in the next 2-3 years from the current level of around 4,000 units, the market size is relatively small when compared to the region (Figure 3). Therefore, it is not yet probable for Thailand to transform itself from a user to industrial robot manufacturer. Instead, it is more possible for Thailand to consider becoming a producer of service robots. The service robot trend is significantly increasing as Thailand is becoming an aging society, the manufacturing sector is extending businesses to the service sector, and consumers are changing their behaviors as previously mentioned. In addition, Thailand is equipped with the required human capital and skills as reflected by projects and awards won by Thai students in various global-level robotics competitions. What is needed is support from all relevant entities to improve and extend such projects to serve commercial purposes. This is will be one important factor in driving and capitalizing on opportunities for Thailand’s robotics industry.

Implication

*

EIC suggests producers of service robots focus on niche markets and aim to increase exports for economies of scale. Take the case of Thailand’s DINSAW robot. DINSAW is a successful case of robotics development with a clear marketing strategy and the right direction to serve the service sector and a focus on the market for the elderly. There is also a target to penetrate overseas markets in Japan and Sweden to boost confidence in the products and gain trust from customers. If successful, DINSAW robots can also expand to other destinations and further exploit economies of scale.

*

Producers of industrial robots should quickly form an alliance with key players to cover the Asian region and develop a strong supply chain. The key industrial robot makers are now in the West. Yet, considering market growth potential and transforming into a robot maker in the future, major players in Asia are important to Thailand in the form of an alliance, instead of competing against each other. Moreover, the region is equipped with supply chains for other industries that are ready to move towards a robotics industry, such as automotive parts, electrical and electronics parts, and high-tech products.

เริ่มซื้อขาย 24 เม.ย. นี้")

ในไทยจะส่งผลให้เกิดแผนธุรกิจและผลิตภัณฑ์ทางการเงินใหม่")