- Details

- Category: อสังหาริมทรัพย์ฯ

- Published: Saturday, 30 April 2016 17:17

- Hits: 2579

เจาะลึกตลาดอสังหาฯ เอกชนวางหมากรับยอดขายบ้านซึม

Highlight

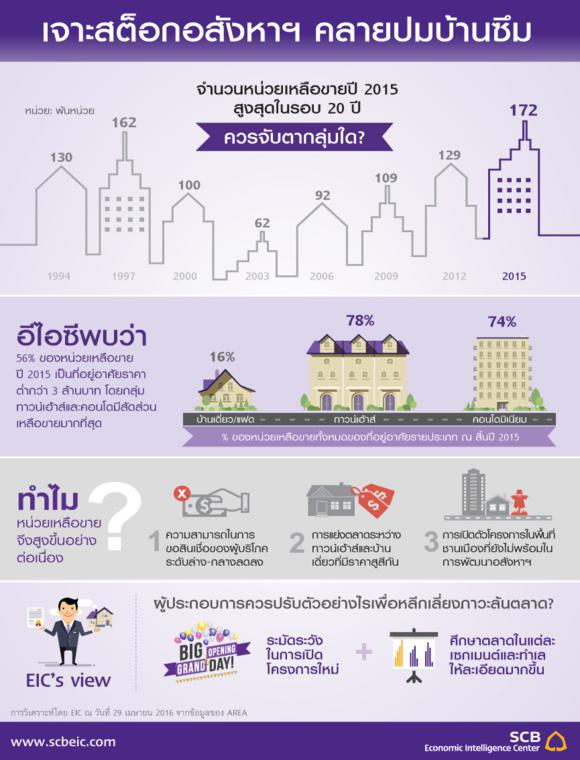

ณ สิ้นปี 2015 จำนวนหน่วยเหลือขายในกรุงเทพฯ และปริมณฑลสร้างสถิติใหม่เกือบ 171,200 หน่วย สูงสุดในรอบเกือบ 20 ปี นับตั้งแต่วิกฤติเศรษฐกิจปี 1997 โดยสาเหตุของจำนวนหน่วยเหลือขายที่เพิ่มขึ้น ส่วนหนึ่งมาจากการเปิดตัวโครงการจำนวนมากในช่วงที่ผ่านมา การนำเอาหน่วยเหลือขายที่ผู้ซื้อไม่ผ่านการอนุมัติขอสินเชื่อมาขายใหม่ และสภาวะการแข่งขันระหว่างที่อยู่อาศัยต่างประเภทในพื้นที่เดียวกันที่เริ่มเห็นชัดมากขึ้น ยกตัวอย่างเช่น ทาวน์เฮ้าส์และบ้านเดี่ยวในบางพื้นที่มีราคาที่ใกล้เคียงกันมากขึ้น เป็นต้น

คาดว่า การส่งเสริมการขายจะยังคงมีการแข่งขันกันค่อนข้างสูง ประกอบกับหากมีมาตรการภาครัฐเสริมจะยิ่งช่วยกระตุ้นเศรษฐกิจ และส่งผลให้ตลาดคึกคักมากขึ้น อีไอซีแนะว่าผู้ประกอบการควรระมัดระวังการเปิดโครงการใหม่ และศึกษาตลาดในแต่ละเซกเมนต์ให้ละเอียดมากขึ้น เพื่อหลีกเลี่ยงและป้องกันภาวะที่อยู่อาศัยล้นตลาด

หน่วยเหลือขายมีจำนวนมากที่สุดในรอบ 20 ปี คอนโดมิเนียมมีหน่วยเหลือขายมากที่สุด คือ 67,349 หน่วย บ้านเดี่ยวและบ้านแฝด และทาวน์เฮ้าส์มีจำนวนหน่วยเหลือขายใกล้เคียงกันคือ 50,909 และ 48,999 หน่วย ตามลำดับ (รูปที่ 1) หากแบ่งตามระดับราคาพบว่า ส่วนใหญ่จะมีราคาต่ำกว่า 2 ล้านบาท ซึ่งมีสัดส่วนถึง 33% ของตลาดโดยรวม รองมาเป็นระดับราคา 2-3 ล้านบาท มีสัดส่วน 24% ของตลาดโดยรวม ทั้งนี้ ด้วยมาตรการภาครัฐที่ให้สิทธิประโยชน์ทางภาษีเพิ่มเติมสำหรับที่อยู่อาศัยไม่เกิน 3 ล้านบาท นับว่าช่วยกระตุ้นยอดโอนกรรมสิทธิ์ในเดือนพฤศจิกายนและธันวาคมถึง 37%YOY และ 52%YOY ตามลำดับ จนทำให้ยอดโอนทั้งปีที่ผ่านมา เติบโตขึ้นถึง 13%YOY หรือ 196,095 หน่วย ซึ่งถือว่าสูงสุดในประวัติการณ์ อย่างไรก็ตาม จำนวนหน่วยที่โอนในเดือนมกราคมปีนี้ กลับลดลง 10%YOY โดยบ้านเดี่ยวและทาวน์เฮ้าส์มียอดโอนลดลงมากสุดถึง 32%YOY และ 22%YOY ตามลำดับ

ภาวะเศรษฐกิจที่ฟื้นตัวช้าส่งผลต่อความสามารถทางการเงินของผู้ซื้อที่อยู่อาศัยระดับล่าง ซึ่งมีการเปิดขายจำนวนมากในหลายปีที่ผ่านมา ผลักดันให้หน่วยเหลือขายสะสมพุ่งสูงขึ้น ทั้งนี้ เนื่องจากผู้ซื้อหลายรายมีคุณสมบัติไม่เพียงพอต่อการอนุมัติสินเชื่อของสถาบันการเงิน ทำให้บางส่วนถูกปฏิเสธ ส่งผลให้จำนวนที่อยู่อาศัยส่วนนี้ต้องนำกลับมาขายในตลาดอีกครั้ง โดยหน่วยเหลือขายของตลาดทาวน์เฮ้าส์และคอนโดมิเนียมที่มีราคาต่ำกว่า 3 ล้านบาท คิดเป็นสัดส่วนถึง 78% และ 74% ตามลำดับ ขณะที่หน่วยเหลือขายของตลาดบ้านเดี่ยวและบ้านแฝดที่ราคา 3-5 ล้านมีสัดส่วนเกือบ 50%

ทาวน์เฮ้าส์แถบชานเมืองมีแนวโน้มขายได้ช้าลงเนื่องจากมีโครงการบ้านที่มีราคาใกล้เคียงอยู่ในทำเลเดียวกัน ยกตัวอย่างเช่น บริเวณหทัยราษฎร์และบางบัวทอง อัตราการขายบ้านเดี่ยวและบ้านแฝดโดยเฉลี่ยจะสูงกว่าทาวน์เฮ้าส์ในทุกระดับราคา บ้านในพื้นที่บริเวณหทัยราษฎร์และบางบัวทองจะขายได้ประมาณ 5% ต่อเดือน ในขณะที่ทาวน์เฮ้าส์ในหทัยราษฎร์จะขายได้ 4% ต่อเดือน และบางบัวทอง 3% ต่อเดือน อีกทั้ง ยังมีโครงการจากผู้ประกอบรายใหญ่และรายย่อยท้องถิ่นหลากหลายให้เลือก ดังนั้น ด้วยสภาวะการแข่งขันที่ค่อนข้างรุนแรงเช่นนี้ ประกอบกับความต้องการซื้อบ้านที่มีทิศทางเดียวกันกับเศรษฐกิจที่ชะลอตัวลง ทำให้หน่วยเหลือขายของทาวน์เฮ้าส์ในแถบชานเมืองมีแนวโน้มค่อนข้างสูง เมื่อเทียบกับบ้านเดี่ยวที่พัฒนาออกมาขายในระดับราคาใกล้เคียงกัน ด้วยเหตุนี้ การพัฒนาโครงการทาวน์เฮ้าส์ใหม่ๆ ในแถบชานเมืองจึงอาจจะต้องระมัดระวังและศึกษาตลาดให้ละเอียดมากขึ้น

ส่วนพื้นที่ในแถบชานเมืองที่รอการขยายตัวจากตัวเมืองสู่รอบนอกอย่างต่อเนื่องในอนาคตอาจจะไม่พร้อมกับการพัฒนาที่อยู่อาศัย ซึ่งอาจจะต้องใช้เวลาอีก 2-3 ปีในการกระตุ้นความต้องการที่อยู่อาศัยในละแวกนั้น แม้ว่าบางพื้นที่จะมีสาธารณูปโภคและสิ่งอำนวยความสะดวกครบครัน รวมทั้งระบบคมนาคมที่ได้รับการพัฒนาอย่างต่อเนื่อง เช่น ไทรน้อย-สุพรรณบุรี แต่เนื่องจากยังมีที่ดินเปล่าซึ่งอยู่ในพื้นที่บริเวณใกล้ตัวเมือง และการเสนอราคาขายที่ไม่ได้แตกต่างกันมากนัก ทำให้ผู้ซื้อเลือกซื้อที่อยู่อาศัยใกล้บริเวณเขตเมืองมากกว่า นอกจากนี้ ผู้ประกอบการบางรายซึ่งเป็นรายย่อยและรายใหม่ที่มีประสบการณ์ในการทำธุรกิจด้านพัฒนาอสังหาฯ ค่อนข้างน้อย บางรายนำที่ดินมรดกมาพัฒนาโครงการที่อยู่อาศัย เพื่อประหยัดต้นทุนที่ดิน แต่อาจจะไม่ได้คำนึงว่าที่ดินดังกล่าวตั้งอยู่ในซอยหรือไกลจากถนนหลักหรือสถานีรถไฟฟ้าที่มีโครงการของผู้ประกอบการรายใหญ่ตั้งอยู่ ทำให้หลายโครงการมีหน่วยเหลือขายในสัดส่วนสูง เมื่อเทียบกับโครงการอื่นๆ ในพื้นที่เดียวกัน ซึ่งอาจจะต้องใช้เครื่องมือทางการตลาดในการขายโครงการและระบายหน่วยเหลือขายให้เร็วขึ้น

อย่างไรก็ตาม อัตราการดูดซับของตลาดโดยรวมในปัจจุบันยังแข็งแกร่งกว่าในอดีตมาก หากเปรียบเทียบกับช่วงวิกฤติเศรษฐกิจ ในปี 1996 อัตราการดูดซับลดต่ำลงจาก 39% จนเหลือ 14% ในปี 1999 ในขณะที่อัตราการดูดซับในปัจจุบันอยู่ที่ 38% ซึ่งสูงกว่าเท่าตัวและสูงกว่าค่าเฉลี่ยของตลาดที่ 37% (รูปที่ 2) คาดว่าส่วนหนึ่งเป็นผลมาจากมาตรการกระตุ้นตลาดอสังหาริมทรัพย์ในช่วงปลายปีที่ผ่านมาที่ทำให้ยอดโอนกรรมสิทธิ์เพิ่มขึ้นมาก อีไอซีมองว่าสภาพตลาดที่อยู่อาศัยในปัจจุบันยังขยายตัวได้ โดยการระบายหน่วยที่อยู่อาศัยอาจจะต้องใช้เวลามากขึ้น ทั้งนี้ ยังคงต้องจับตามองตัวเลข NPL ของสินเชื่อเพื่อที่อยู่อาศัยที่ปัจจุบันยังมีสัดส่วนไม่มากนัก แต่ก็มีแนวโน้มเพิ่มขึ้น นอกจากนี้ ยังคงต้องจับตามองหน่วยที่คาดว่าจะก่อสร้างแล้วเสร็จในอนาคต โดยเฉพาะปี 2017-2018 ที่คาดว่าจะมีจำนวนสูงกว่าปีนี้ ด้วยสัดส่วน 31% และ 5% ตามลำดับ (รูปที่ 3) ซึ่งจะส่งผลให้มีหน่วยเหลือขายสะสมเพิ่มขึ้นอีก

นอกจากนี้ การปรับตัวของผู้ประกอบการที่ชะลอการเปิดโครงการใหม่ ประกอบกับสถานะทางการเงินที่มั่นคง ทำให้สภาวะตลาดยังไม่น่ากังวลมากนัก อัตราส่วนหนี้สินต่อทุนที่อยู่ในระดับต่ำ สะท้อนให้เห็นความแข็งแรงทางธุรกิจของผู้ประกอบการ โดยปัจจุบัน อัตราส่วนหนี้ต่อทุนของผู้ประกอบการซึ่งพัฒนาที่อยู่อาศัยที่อยู่ในตลาดหลักทรัพย์เฉลี่ยอยู่ที่ 0.78 เท่า ต่ำกว่าช่วงวิกฤติเศรษฐกิจที่ระดับ 2.33 เท่า อยู่มาก นอกจากนี้ ผู้ประกอบการมีการปรับตัวให้สอดคล้องกับสภาวะเศรษฐกิจที่เปลี่ยนแปลงไป โดยศึกษาตลาดและพฤติกรรมผู้บริโภคมากขึ้น ดังนั้น ตลาดที่อยู่อาศัยในกรุงเทพฯ และปริมณฑลจึงยังไม่อยู่ในภาวะที่น่ากังวล

Implication

คาดว่าการส่งเสริมการขายของผู้ประกอบการจะยังมีการแข่งขันรุนแรง ซึ่งหากมีมาตรการภาครัฐเข้ามาช่วยเสริม จะทำให้ตลาดที่อยู่อาศัยคึกคักและกระตุ้นเศรษฐกิจได้มากขึ้น ที่ผ่านมามาตรการภาครัฐช่วยกระตุ้นยอดโอนได้สูงขึ้นโดยเฉลี่ยประมาณ 10% ทั้งนี้ คาดว่าผู้ประกอบการจะยังมีกลยุทธ์หรือการส่งเสริมการขายมากขึ้นในหลายรูปแบบ เช่น การให้ส่วนลดราคาในรูปแบบต่างๆ อย่างไรก็ตาม ผู้ประกอบการควรระมัดระวังการเปิดขายโครงการใหม่ให้มากขึ้นเพื่อให้ตลาดได้ระบายหน่วยเหลือขายสะสมก่อน และป้องกันปัญหาขาดแคลนสภาพคล่องทางการเงินของผู้ประกอบการเองด้วย

ผู้ประกอบการควรศึกษาตลาดในแต่ละเซกเมนต์ให้ละเอียดมากขึ้นในการจะเปิดโครงการใหม่ เพื่อป้องกันภาวะที่อยู่อาศัยล้นตลาด ทั้งนี้ แม้ตลาดที่อยู่อาศัยจะยังไม่น่ากังวลมาก เมื่อเทียบกับช่วงวิกฤติต้มยำกุ้ง และผู้ประกอบการมีฐานะทางการเงินที่ดีกว่า แต่อัตราการขายก็ค่อนข้างชะลอตัวลงตามภาวะเศรษฐกิจ โดยผู้ซื้อส่วนใหญ่มีการวางแผนทางการเงินที่รอบคอบและตัดสินใจซื้อที่อยู่อาศัยยากขึ้น ดังนั้น ผู้ประกอบการควรมีการปรับตัวตาม โดยศึกษาสภาวะตลาดและความสามารถของผู้ซื้อมากขึ้น

Cracking house stocks and rolling out new strategies

Highlight

At the end of 2015, the number of unsold residential units in the Bangkok Metropolitan Region (BMR) reached 171,200 units, the highest level since the 1997 Asian financial crisis. The increasing number of unsold vacancies is partly due to the high number of new housing projects and the resale of units that could not be transferred because the initial buyers were denied housing loan approval. This oversupply increases competition, not only within the same market segments, but also between similarly-priced townhouses and houses in some areas.

Sales promotion will intensify competition for the real estate market. Government’s stimulus measures could boost the efficiency of the market. EIC suggests that residential developers should launch new project carefully and conduct a deep-dive market study in each segment to avoid the risks of excessive house supply.

The number of unsold residential units has reached the highest level in 20 years. Most of the vacancies are in condominiums, with 67,349 unsold units. Unsold detached and semi-detached houses tally 50,909 units, similar in number to the 48,999 units of unsold townhouses (Figure 1). Categorizing by price, we find that many unsold units are priced below 2 million baht. This group accounts for 33% of the real estate oversupply, while units priced between 2-3 million baht account for 24%. The ongoing oversupply comes despite the government’s property stimulus package especially targeting units priced below 3 million baht. The stimulus measures, including various tax benefits, increased the number of housing transfers in November and December by 37% YOY and 52% YOY respectively, leading to record breaking growth in total transfer value of 13% YOY, an increase of 196,095 units in 2015. The number of units transferred in January 2016, however, dropped 10% YOY owing mainly to the 32% YOY decrease in detached house transfers and a 22% YOY drop in condominiums transfers.

A slow economic recovery has affected the purchasing power of the low-income group, a target group for many recently opened residential projects, adding to the accumulation of unsold properties. Moreover, many home buyers are not qualified for loans, so financial institutions deny their mortgage applications, resulting in re-sales. The proportions of unsold townhouses and condominiums priced less than 3 million baht are 78% and 74%, respectively. At the same time, unsold detached and semi-detached houses priced at 3-5 million baht account for almost 50% of unsold detached and semi-detached houses units.

Suburban townhouse sales will likely stall due to similarly-priced houses in the same area, for example, around the Hatairat and Bang Bua Thong areas. The average number of houses sold is higher than townhouses at every price level. In the two areas mentioned above, the rate of house sales is about 5% per month, while townhouses sell 4% per month in Hatairat and 3% per month in Bang Bua Thong. The close numbers of available house and townhouse units and the diversity of residential choices provided by both larger and local developers have raised competition in the suburban housing market. With the steep competition and weak property demand from a lackluster economy, the suburban townhouse market will likely be left with many unsold units compared to similarly-priced detached houses. Suburban townhouse developers should be careful and study the market in detail before proceeding.

City fringes, yet to be expanded upon, might not see enough demand for real estate development until the next 2-3 years. Although equipped with public utilities and other amenities as well as the ongoing development of the public transport system, outlying areas such as Sai Noi - Suphan Buri are being neglected by home buyers since areas closer to the city still have available patches of land waiting to be developed and the prices of the currently available residential units do not differ that greatly from those further away from the city. Moreover, some of the existing developers in the area are new to the real estate business with little experience and are smaller in size. Some use inherited land to reduce costs but inherited estate is usually located in soi areas or far away from main roads or city rail routes, areas already occupied by larger developers. Projects further away, therefore, have higher numbers of unsold units compared to other projects in the same areas. Developers should look into marketing tools to boost sell these unsold vacancies at a quicker rate.

Nonetheless, the current absorption rate of overall market is much stronger than in the past. During the crisis, the absorption rate declined from 39% in 1996 to 14% in 1999. On the contrary, the current absorption rate stands at 38%, more than twice of 1999 and also higher than the market average at 37% (Figure 2). This is partly due to the high volume of transferred units, boosted by the government's stimulus package late last year. EIC therefore foresees that there is still room for expansion in the residential market, although it will require more time to clear unsold stock. The number of non-performing housing loans should be monitored as it has been climbing since 2010, although currently not very high. Developers should also watch for construction scheduled to start in the future, especially during 2017-2018. Compared to this year, the expected number of completed condominiums in 2017 and 2018 will be 31% and 5% higher, respectively (Figure 3).

Furthermore, delayed launching new projects and solid financial position of developers could indicate no concern in the industry. Low debt-to-equity ratios generally indicate strong financial positions. Average debt-to-equity ratios of listed real estate developers is 0.78, much lower than the ratio of 2.33 during the crisis. Moreover, developers tend to study and analyze market structures and consumer behaviors, so that they could adjust the business plans that align with current economic constraints. Therefore, the real estate market in Bangkok and metropolitan areas has no particular worrisome condition.

Implication

The market could expect to see the intensified competition with harder sales promotions which the government’s property measures to be entitled to boost the market and entire economy. Previous government stimulus measures increased the volume of transferred units by 10%, on average. EIC expects developers to level up strategies and sales promotions, such as discount campaigns. Developers should, however, refrain from launching new projects to allow the market to first clear some of the unsold units and to avoid having insufficient financial liquidity.

Developers should stay cautious in launching new projects, and study the markets in each segment and deep details since the real estate cycle seems to be transitioning to a hyper-supply phase. After the 1997 financial crisis, the market took six years to absorb unsold vacancies from 162,000 units in 1997 to 62,000 units in 2003 before starting to accumulate unsold units again, reaching the highest number this year. However, current economic conditions differ from those of 1997 and buyers are also more cautious financially and more careful with their property buying decisions. Developers should therefore adjust to changing market conditions and purchasing powers.

ตรวจความพร้อม รถไฟทางคู่ช่วงมาบกะเบา-ชุมทางถนนจิระ")

ตรวจความพร้อม รถไฟทางคู่ช่วงมาบกะเบา-ชุมทางถนนจิระ")